SME Invoice Finance

Release instant cash from unpaid invoices

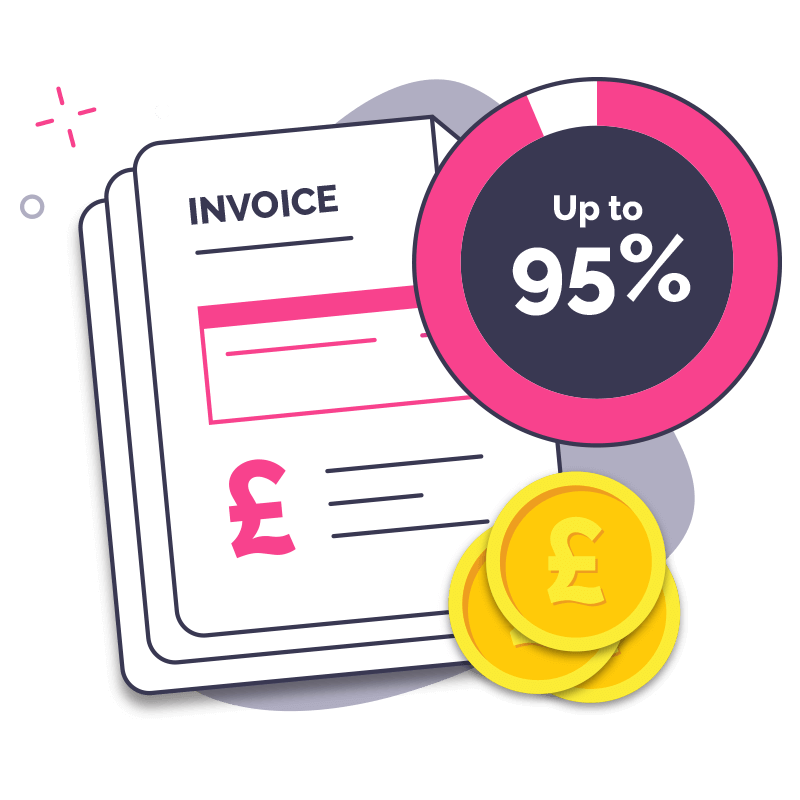

- Receive up to 95% of invoice value

- Sell single or multiple invoices

- Fast, stress-free funding in 24 hours

Quick Decision with No Obligation

Release instant cash from unpaid invoices

Quick Decision with No Obligation

Open up to a new world of stress-free cash flow with invoice finance. By converting your invoices into cash, you will have a more efficient cash flow system enabling you to trade without the constraints of slow-paced debtors.

By unlocking cash within your business invoices, you can release large amounts of money upfront.

Whether you want to use a single invoice or your full sales ledger, we have a flexible finance solution to suit your business.

Get the money in your account within 24 hours after approval.

Invoice finance frees up your money almost instantly. You don't have to wait weeks or months for clients to pay.

A confidential discounting service is available, meaning your clients won’t see any difference to your service.

Free up time to manage your business utilising sales ledger management & debt collection processes.

Quick Decision with No Obligation

Some of the funders we work with

An invoice finance facility gives your SME business the immediate working capital it needs by simply selling raised, unpaid invoices in return for a lower cash value. These facilities can be tailored to your needs, with the option to retain or outsource full control of your sales ledger and relationships with your customers.

Sell your products or services to business customers as usual and issue invoices with a 30 to 90-day payment term.

Once your facility is set up, you can choose one invoice, multiple invoices or your full sales ledger to release cash against. The invoice financier will simply 'buy' the debt that is owed by your customer.

Receive an invoice advance up to 95% of the value of your sales invoices in 24 hours.

When the invoice is due, the client pays the invoice to the invoice finance providers account.

Depending on the facility you have chosen, the provider can manage the sales ledger, credit control and chasing customer payments on your behalf, or it can remain with you.

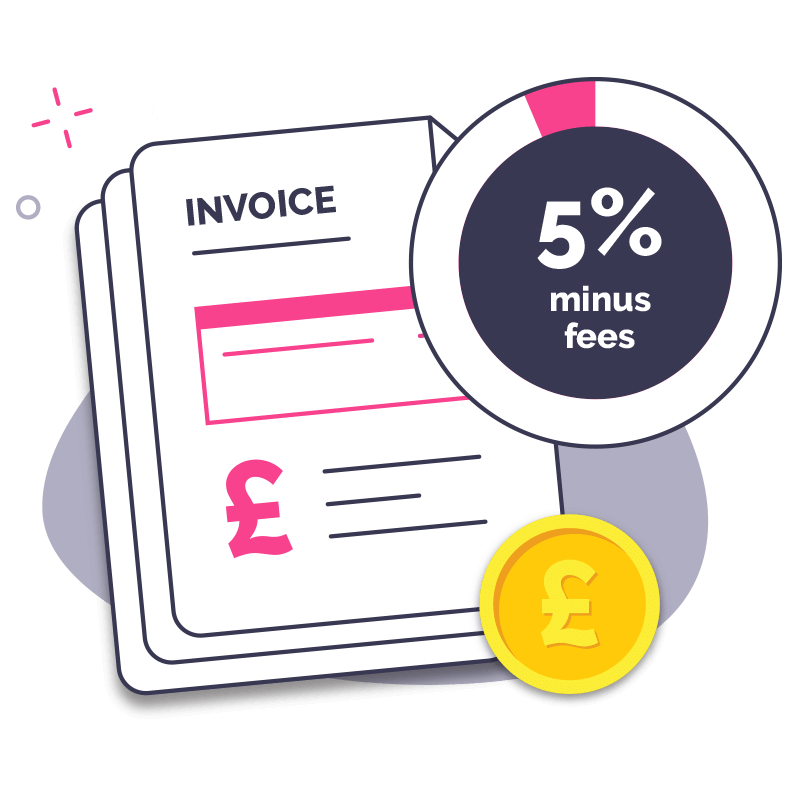

Compare FacilitiesYou will then receive the remaining balance, minus any fees and charges agreed with the invoice finance provider.

Get your free, tailored, no-obligation quote today

Apply NowQuick Decision with No Obligation

There are different variations of invoice finance that are designed to meet different business requirements. The two most popular types of SME invoice finance are invoice discounting, in which the business retains management of its sales ledger in a confidential arrangement, and invoice factoring, that hands over credit control to the finance provider, who will collect on payments from debtors.

Access funding while managing your own credit control – 100% confidential service.

Learn MoreFull credit control and sales ledger management with funding and collection service.

Learn More| Compare | Discounting | Factoring |

|---|---|---|

| Can I release up to 95% in 24 hours? | ||

| Are credit control services provided? The provider manages sales ledger and invoice collection on your behalf. |

||

| Is it confidential? Confidentiality means that customers will not know you are using a facility. |

Quick Decision with No Obligation

Unlike many other business finance products on the market, invoice financing delivers the funds quickly, in as little as 24 hours after approval.

Working with many types of businesses from small start-ups to larger, established corporate enterprises, we have an SME invoice finance solution that can be tailored to your specific requirements.

Quick Decision with No Obligation

Since 2014, we've helped many businesses, large and small, get access to the working capital they need through invoice financing.

33,000+

SME's use invoice finance to help with growth*

£21.5 billion

Total amount funded to businesses across the UK*

£313 billion

Supporting a combined total business turnover per year*

*According to UK Finance statistics for the full calendar year to 31st December 2024.

Invoice financing allows businesses to borrow against the value of their unpaid customer invoices. By selling invoices to a third party, you can unlock immediate access to funds without having to wait for customers to pay the invoice, helping with cash flow and supporting growth.

Invoice financing can be a good idea for small and large businesses that need to access large amounts of cash tied up in their unpaid invoices. Here are just some of the benefits of invoice finance:

Eligibility factors can vary from different providers, but you should qualify for invoice financing if :

It is worth noting that some providers may only accept businesses with a minimum turnover per annum and minimum monthly invoices sent per month.

To check if your business qualifies for invoice financing, simply apply now, and our team will be happy to help.

Unlike a traditional loan, invoice finance is an effective form of borrowing money without feeling like you're borrowing money. It's an advance of the money that's owed to you. You pay a small fee to the lender to receive all of that money.

Keeping a healthy cash flow when you're in business isn't easy at all times. So it's great to have an alternative route to funding that keeps your business running smoothly.

Most providers assign a dedicated account manager to deal with your business. You can also have real-time access to your account to see what funds are available to you and withdraw.

This will depend on the type of invoice financing facility you choose. For a continuous invoice finance facility like factoring or discounting, it's common to be on a six month or yearly contract. Some providers offer a trial period for a contracted service. However, selective invoice finance providers can work on a 'pay as you go' method with no contracts.

Many businesses find it hard to gain funding such as traditional lending from the bank. You are not judged on your historical financial performance but the ability to make sales and retain customers.

You're in control of how many invoices you submit, so you know how much could be eligible for the advance. This means you can predict your cash flow for the coming months.

Most invoice finance providers offer Bad Debt Protection. This safeguards you and your business against any potential losses caused by a customer not being able to pay. Make sure it's one of their priorities, as you'll need it if you find yourself with a problematic customer.

If you opt for a factoring facility, the invoice finance provider will manage your credit control, and your customers will be aware of your relationship with the provider. Lots of finance providers have specialised and trained teams to deal with your customers. Many find that the transaction becomes seamless, meaning you get happier customers who pay on time.

The cost will depend on the type of invoice finance agreement and the provider you choose. Typically, you will pay:

Some providers have no setup fees and only take a finance fee once they have secured payment from your customer. Other providers charge a setup and service fee for outstanding invoices.

When researching providers, you'll want to know what costs are involved for the duration of your contract. Why not apply now to get your free, tailored, no-obligation quote today!

If you have raised an invoice to your customer in the early months of your startup, then you will be eligible for this type of funding. If you are at a pre-revenue stage, you won't be eligible until you start billing your customers. However, many providers offer other forms of business finance to start up businesses; you just need to find out if they are the right fit for you.

Providers need to make their checks before opening an account, but if you sail through the process, you could open your account within days and start receiving advances after sending over your first invoice.

The Financial Conduct Authority (FCA)

The FCA is an independent, non-governmental body that regulates the UK financial services industry. They regulate many products within the business finance industry, but currently they do not regulate invoice finance.

UK Finance (formerly ABFA)

UK Finance recently integrated Asset Based Finance Association (ABFA) into their new trade association, representing more than 300 UK credit providers, including invoice finance companies. All Invoice Finance and Asset Based Lending (IFABL) members adhere to standards and code of practice.

We can help any UK business that invoices other companies on credit terms for the goods and services that they provide.

Get your free, tailored, no-obligation quote today

Apply NowQuick Decision with No Obligation